How to Pay Off Credit Card Debt Fast

In today's rapidly evolving financial landscape, managing credit card debt efficiently has become a crucial skill. The allure of credit ...

In today's rapidly evolving financial landscape, managing credit card debt efficiently has become a crucial skill. The allure of credit ...

In today's world, student loans have become a crucial means of financing higher education. With the increasing cost of college ...

In today's financial landscape, managing personal debt has become increasingly crucial as individuals grapple with student loans, credit card balances, ...

Mortgage Prepayment: Is It a Smart Financial Move?

Stop Living Paycheck to Paycheck: A Simple Guide to Financial Freedom

Your Credit Score, Explained: What Is It and How to Improve It

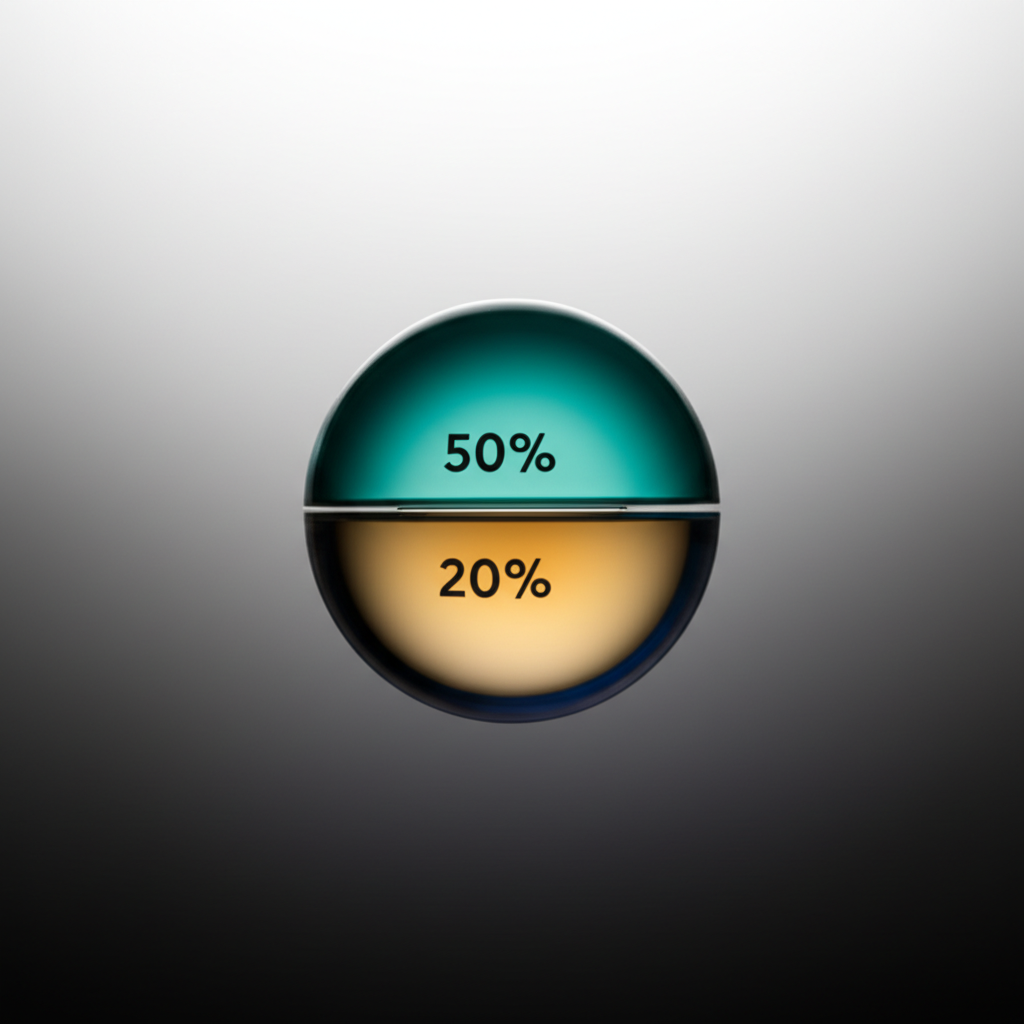

The Ultimate Guide to the 50/30/20 Budget Rule

In today's fast-paced financial landscape, individuals are increasingly motivated to achieve significant goals like vacations, home purchases, and more. These ...